Four consecutive years of high double-digit returns in the stock market is a rare occurrence. Indeed, it’s happened once in 100 years. If this year ended on a high, it would be the second time investors enjoyed four consecutive high-returning years.

A growing number of reputable investors, however, are suggesting that the outcome is unlikely and they’re citing the relentless rise of sovereign bond yields.

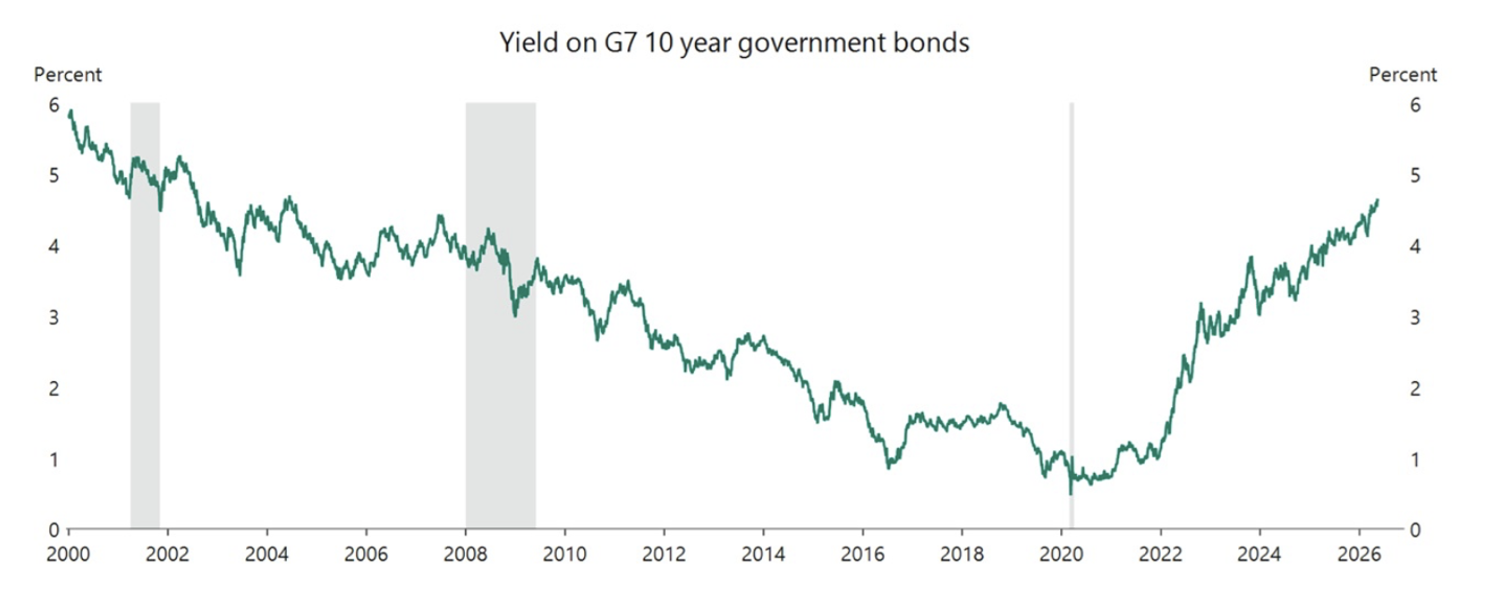

According to Torsten Sløk, chief economist at Apollo Global Management, government bond yields across the Group of Seven (G7) nations have surged to their highest levels since 2004.

Figure 1. G7 Government bond yields highest since 2004 (22 years)

Source: Apollo Global Management

The milestone has sparked widening concern among analysts that the equity market has entered the potentially volatile late stages of a speculative boom. The prevailing view among a growing chorus of bearish predictions is that soaring risk-free rates and a staggering mountain of public debt, particularly in the U.S., pose a direct threat to equity valuations.

Since the Global Financial Crisis (GFC), artificially suppressed interest rates acted as a powerful tailwind for equities, pushing investors into riskier assets on the assumption that There Is No Alternative (TINA). Today, however, fixed-income securities are offering a highly competitive haven for investor capital.

To understand why elevated bond yields should trouble stock market investors, you have to consider the mechanics of asset pricing. Financial markets operate under the laws of what Warren Buffett once referred to as economic “gravity”, where government bond yields dictate the baseline cost of capital.

When risk-free sovereign bonds offer yields near five per cent, the hurdle rate for investing in stocks rises dramatically. Institutional investors are less incentivised to absorb equity market volatility and risk when they can lock in historically high, guaranteed returns backed by sovereigns with the power to tax their constituents to raise revenue (as we are discovering in Australia!).

Furthermore, higher bond yields impair equity valuations through the discounted cash flow calculation. The present value of future corporate earnings is calculated using a discount rate heavily tied to prevailing treasury yields. As yields climb, this discount rate spikes, automatically compressing forward price-to-earnings (P/E) multiples. This valuation compression severely damages high-growth sectors like technology, where projected cash flows lie out in the distant future. Consequently, even if earnings remain healthy, rising capital costs force a downward repricing of equities, presenting a structural headwind for stocks – even if earnings are expected to grow.

More importantly, the forces driving yields upward appear to be structural rather than cyclical because they’re tied to expanding government deficits and morphing central bank policies.

It was economist and strategist Ed Yardeni who famously coined the term “bond vigilantes” to describe investors who sell bonds to protest inflationary fiscal policies. Yardeni, a noted stock market bull, has admitted that these bond market actors are actively forcing the hands of policymakers.

In the wake of escalating geopolitical tensions, including the closure of the Strait of Hormuz and consequent resurgence in global energy prices, headline inflation is proving stubbornly uncooperative. In fact, the U.S. Federal Reserve’s preferred inflation gauge – the Personal Consumption Expenditures (PCE) price index – last sat below its 2 per cent target in February 2021. That’s over five years since PCE inflation was below 2 per cent.

The bond market has reacted by demanding a significantly higher inflation risk premium, pushing yields to levels that directly challenge Trump, and by extension, the Fed’s agenda – to lower rates.

One interpretation of rising bond yields, and in particular the yield curve flattening we are seeing, is that bond traders -Yardeni’s ‘vigilantes’- are effectively forcing the Federal Reserve to abandon its accommodative bias in favour of a prolonged tightening stance, locking the economy into a higher-for-longer interest rate regime that must sap equity market liquidity.

Meanwhile, Ray Dalio, the billionaire founder of Bridgewater Associates, and something of a market and economic Cassandra, views the current turbulence through a different lens – one that prioritises long-term debt cycles. Dalio reckons the United States must navigate debt saturation, which is the consequence of massive structural deficits that require an unprecedented volume of new debt to be issued. With nearly US$10 trillion dollars of American public debt requiring rollover in the near term, Dalio suggests the sheer supply-and-demand imbalance threatens to destabilise the financial system.

Dalio worries that foreign buyers will reduce their appetite for American sovereign debt amidst rising geopolitical fragmentation and a creeping capital war. Either bond yields have to spike higher to attract capital, or the central bank will be required to print money, triggering further rises in inflation as well as severe currency debasement.

In either scenario, equities are less attractive, just as long-term debt assets look unappealing, creating an environment in which equity risk premiums (the extra return an investor expects to receive for choosing to buy ‘risky’ stocks instead of safe, risk-free government bonds) have become unsustainably compressed – you’re just not being offered enough ‘extra’ return for being in stocks.

And then there’s Michael Burry, the contrarian investor renowned for predicting, and profiting from, the 2008 subprime mortgage crisis, whom I wrote about recently here: Yardeni vs. Burry – The Bull vs the Bear.

The parallels between current market euphoria and previous episodes that produced historic speculative collapses have caught Burry’s attention. Burry warns today’s market echoes the peak of the dot-com bubble. While the public has been captivated by an artificial intelligence (AI) driven boom, the underlying reality is a market trading at extreme valuation multiples completely disconnected from historical norms.

Burry further points out that speculative frenzies depend on cheap, abundant leverage. With borrowing costs now rising and potentially rising permanently, the structure supporting these inflated stock prices unwinds. Rising interest rates act as the ultimate pin that pricks speculative bubbles, and this has seen Burry to publicly shift his own capital away from overextended technology mega-caps and into uncorrelated, discounted value assets.

While you might not be convinced by Yardeni, Sløck, Dalio or Burry, consider the cautious thesis implied by Warren Buffett’s recent moves.

While Buffett officially transitioned to ‘Chairman Emeritus’ of Berkshire Hathaway at the conclusion of 2025, handing operational control to Greg Abel, his conservative capital allocation philosophy continues. Berkshire Hathaway’s cash pile has reached an astronomical and record-breaking US$397 billion. The cash pile has grown amid a multi-year net liquidation of stocks, which included slashing Berkshire’s stake in Apple and cutting its holdings in Bank of America by more than half. And the cash has been parked in short-term U.S. Treasury bills, capturing a safe, predictable return of four to five per cent, while share buybacks have been halted for nearly two years. What are we to read from this other than Buffett believes stretched equity valuations and high sovereign yields mean risk-free government debt will outperform speculation on an overextended AI-driven stock market.

Can they all be wrong? The short answer is yes. But their track records suggest it’s unlikely they’re all wrong at the same time. Given the era of artificially suppressed interest rates is firmly in the past, and bonds are reclaiming their place as a harbour for global capital the stock market’s recent near vertical ascent seems oddly misplaced. Unless it is a blowoff top, that is.

As long as structural fiscal deficits, geopolitical division, and energy-driven inflation shocks continue to push sovereign yields to multi-decade highs, the stock market’s highs will remain in direct conflict with the laws of gravity.

Perhaps equity investors accustomed to decades of cheap money haven’t read the memo? The transition to realisation could prove expensive and volatile.