Peter Lynch, the legendary investor, once quipped that it’s best to invest in businesses that any idiot could run, because sooner or later one will. This begs the question of what drives the economic returns of businesses: is it the competitive forces of that industry or the skill of management? It’s likely a combination of both.

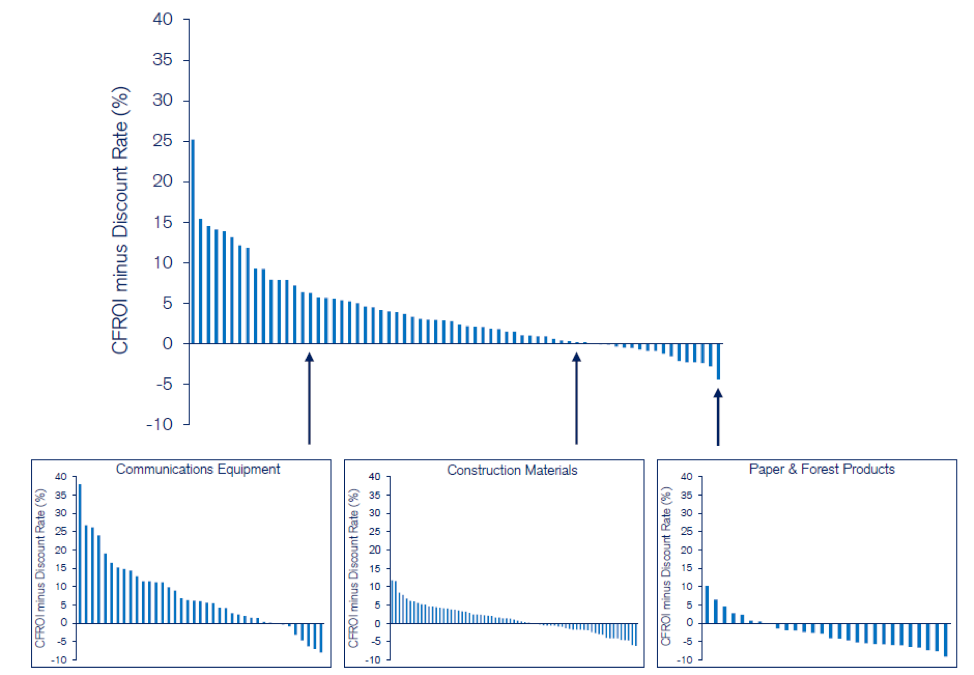

The following graph looks at the distribution of value creation for a range of industries. The blue bars are measuring the spread between the cash flow return on investment (CFROI) and the cost of capital for 68 global industries as defined by MSCI’s GICS system. The data was taken from a sample of 5,500 public companies. The smaller graphs focus on the value creation (or value destruction) for companies within a specific industry.

Source: Credit Suisse HOLT

What we can observe is that on average some industries create business value, and others destroy business value. However, we can see that within any given industry there are firms creating value, and others destroying value. What this means is that even the industries that on average create the most business value contain firms that actually destroy value.

However, there are certain industries where the economics are so challenging that there is little a good management team can do to generate positive economic value. To quote Warren Buffett: “When a management with a reputation for brilliance tackles a business with a reputation for bad economics, it is the reputation of the business that remains intact.”

Take the airline industry for example. The International Air Transport Association estimated that over the 2002-09 business cycle, the airline industry destroyed an average of $19 billion of shareholder capital per annum. Intense competition, high capital expenditures to purchase aircraft, volatile input cost prices (i.e. oil prices) combine to create an industry that has historically struggled to generate positive economic value. While there are players within the airline industry such as travel agents and freight forwarders that generated positive economic value, it was insufficient to offset the value destruction from the airlines.

At Montaka Global we seek to find businesses that are both cheap, and able to reap an outsized share of the industry economics. It is these investments that we believe are likely to have a greater likelihood of performing well for our investors over time.