Small and Medium Enterprises (SMEs) have long been neglected by the banking sector in Australia. The amount of data required to assess the credit, application processing time and associated costs of processing has meant that the banks have pushed SMEs towards real estate backed loans. This does not suit the SMEs in many cases. Given the increased complexity of the credit assessment, many SME loans have higher yields than consumer loans.

In this blog, I explain how this has created a funding gap that SME Alternative Finance (AltFi) lenders are seeking to bridge in order to set the context for the emergence of SME debt capital as an emerging asset class for investors seeking income and returns that have little to no correlation with public markets.

AltFi lenders have developed products that allow SMEs to borrow to match the duration of their funding needs, on an unsecured basis or secured against non-real estate business assets such as invoices or stock. Technology, in particular cloud accounting software and online access to bank account information, has enabled significantly faster credit assessments and reduced funding times for SMEs, opening up an underbanked market within the SME sector. The market opportunity is significant for Fintech enabled SME AltFi lenders.

The main impediment to growth for Fintech enabled AltFi lenders is access to funds to lend to SME borrowers. Banks have proven reluctant to fund these Fintech businesses in recent years potentially due to their relatively short track record or ethical considerations due to perceived higher rates being charged by these lenders.

This opens a yield play for investors and a credit opportunity within global debt markets.

An overview of the Australian SME sector

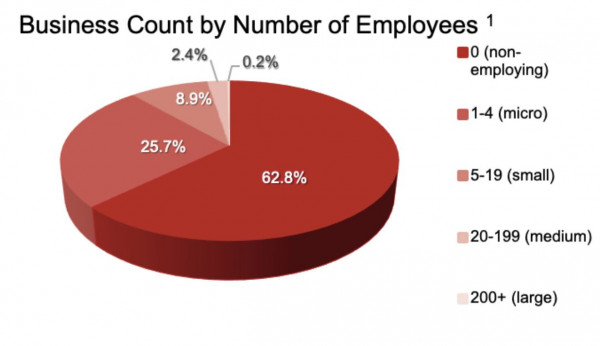

Small business is typically defined as companies who employ 5 – 19 staff and medium-sized business are defined as companies who employ 20 – 199 staff. As of 30 June 2019, there were 212,247 small businesses and 56,835 medium-sized businesses1.

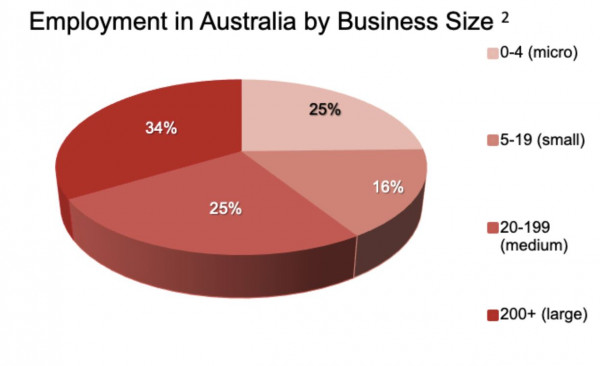

Moreover, as of 30 June 2019, businesses with fewer than 200 employees accounted for 66 per cent of employment.2

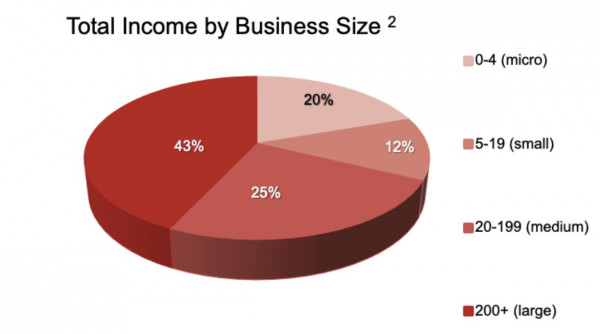

SMEs also account for a significant proportion of private sector income. As at 30 June 2019, private sector income totalled $3.7 trillion, of which small businesses (5-19 employees) accounted for $462 billion and medium businesses (20 – 199 employees) $919 billion.

Small business entrepreneurs will often use their families’ finances to fund their business. Some seek external funding, which can include extra equity or debt from family and friends, debt from financial institutions or equity from venture capital funds. In Australia, the banks’ business models and expertise may be more suited to providing debt finance to established businesses whereas venture capital is more suited to start-up firms in nascent industries.3

The problem - Australian SMEs are not being financed by traditional lenders

Whilst SMEs in Australia continue to make a significant contribution to the economy, they have not been well supported by the banking sector. The main friction points SMEs suffer within the banking sector include:

Banks have been unable to efficiently process the smaller end of the SME credit space as their current processes take time due to the manual nature of information collection and processing. This has led to SMEs seeking out alternative sources to fund their growth.

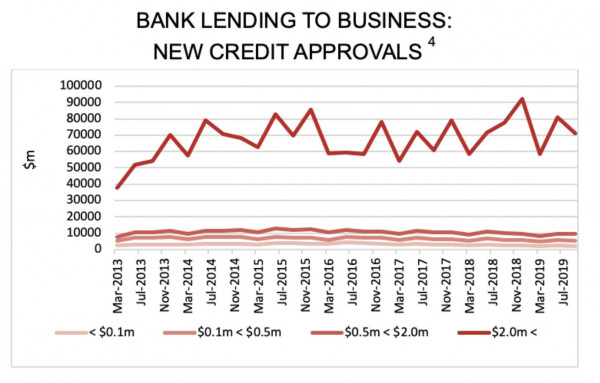

Total bank lending to business new credit approvals4 which represents new loans approved, for the year ended September 2019 for loans under $2 million, amounted to AUD $67.540 billion, down 10.88% and AUD $8.249 billion on the previous 12-month period. Meanwhile, loans over $2 million amounted to AUD $302.835 billion, up 5.59% and AUD $16.032 billion on the previous 12-month period.

The solution - Tech-enabled lenders removing friction for SME borrowers

SME Alternative Finance (AltFi) lenders have been set up to target the underbanked markets within the Australian business landscape to provide financing solutions to Australian SMEs.

The underbanked market includes businesses which have passed on potential growth opportunities due to difficulty in receiving finance, although not necessarily due to poor credit, but potentially due to its lack of size, or where, from the business' perspective, there is a lack of human resources to complete the application process.

Some lenders in the AltFi SME sector use technology applications to collect data from borrowers and monitor the financial health of the business on an ongoing basis, whilst the loan is still live. This allows the lender to have an insight into the ability of the counterparty to repay the loan on an ongoing basis. A further extension to this is the ability to work with the borrower on their forward cash flow projections and tailor funding solutions to the business.

Lenders may use application programming interfaces (APIs) to plug into cloud-based accounting software and bank accounts to share data and reduce much of the friction in the application process, saving time for the borrower and making borrowing funds a less manual and much smoother process.

Overview of the Australian SME AltFi market

According to the Australian Banking Association Economic Report, September 2019; “Australian Banking Association data shows a 33 per cent decline in (SME) business loan approvals over the past five years, while approval rates remain around 94%”.

Given approval rates have remained relatively steady over the past five years, the 33 per cent decline in loan approvals can only be explained by a reduction in loan applications made by SMEs. This data in combination with ABS Counts of Australian Businesses data5 which shows a 6.96 per cent increase in the number of Australian SMEs over the five-year period to June 30 2019, suggests the reduction in applications is not due to an off-setting decline in the number of SMEs. Rather, the data suggests SMEs are looking elsewhere for their funding requirements.

Asset overview & risk-based pricing

Lenders in the SME AltFi sector will predominately apply risk-based pricing to their product set. Risk-based pricing is simply pricing according to the risk of the lender, so a higher rate for a higher risk borrower, and a lower rate for a lower risk borrower. This pricing methodology is not used in the bank models, where rates are offered at each product type.

Loans made by SME AltFi lenders are typically structured in the manner outlined below:

Asset Backed

Unsecured

Closing remarks

The Australian SME AltFi market continues to grow in terms of volumes lent, as SMEs preference for non-banks to fund growth has now surpassed traditional banks. Whilst the banks focus on larger lends, Aura expects this sector to continue to grow. SMEs are actively utilising the greater choice in the funding landscape to support their growth, which is a positive for the wider Australian economy, and the 66% of the workforce that is employed by Australian SMEs.

While SMEs awareness and use of these lending products and lenders have significantly increased in recent years, the primary constraint for the industry is funding for the lenders.

Footnotes

1 8165.0 Counts of Australian Businesses, including Entries and Exits, June 2015 to June 2019

2 8155.0 - Australian Industry, 2018-19 – Table 5

3 Financial System Inquiry, December 2014

4 RBA Bank Lending to Business – New Credit Approvals by Size and by Purpose – D7.4, Aura Funds Management, September 2019

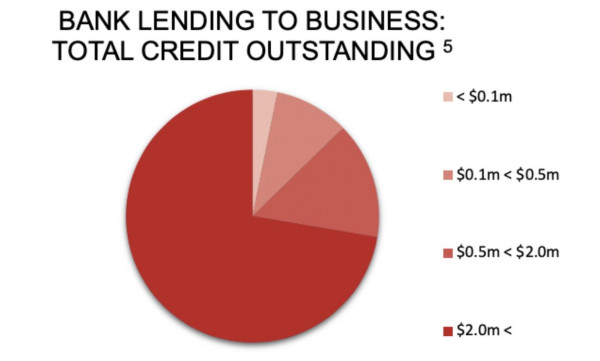

5 RBA Bank Lending to Business – Total Credit Outstanding by Size and by Sector – D7.3, Aura Funds Management, September 2019

This information is for accredited, qualified, institutional, wholesale or sophisticated investors only and is provided by Aura Funds Management Pty Ltd (ABN 96 607 158 814, Authorised Representative No. 1233893 of Aura Capital Pty Ltd AFSL No. 366 230, ABN 48 143 700 887). Aura Funds Management Pty Ltd is the Trustee of all the Funds mentioned and a subsidiary of Aura Group Pty Ltd.

Any financial product advice given in this report is of a general nature only. The information has been provided without taking into account the investment objectives, financial situation or needs of any particular investor. Therefore, before acting on the information contained in this report you should seek professional advice and consider whether the information is appropriate in light of your objectives, financial situation and needs. Aura does not guarantee the performance of its funds, the repayment of any capital or any rate of return. Investing in any financial product is subject to investment risk including possible loss. Past performance is not a reliable indicator of future performance. Information in this report is based on the information provided to Aura by third parties that may not have been verified. Aura believes that the information is reliable but does not guarantee its accuracy or completeness. Aura is not able to give tax advice and accordingly investors should obtain independent advice from an accountant and/or lawyer before making any decision based on the tax treatment of its investors.

You must read the Fund Fact Sheet or Information Memorandum and seek professional advice before making a decision to invest in any of the funds.