Indicators worldwide continue to reflect the damaging effects of the coronavirus pandemic and associated restrictions on economic activity and business profits. Yet puzzlingly equity markets have continued to rise. This suggests that the equity market does not seem to care about earnings – yet. History shows that in the long run earnings will still matter.

In a recent interview with the Economic Club of New York, Stanley Druckenmiller said “in the intermediate term liquidity moves markets more than earnings.” Druckenmiller, known as one of the world’s greatest investors, pointed to the massive liquidity injection by the Federal Reserve Bank as the main reason for a rebound in stocks.

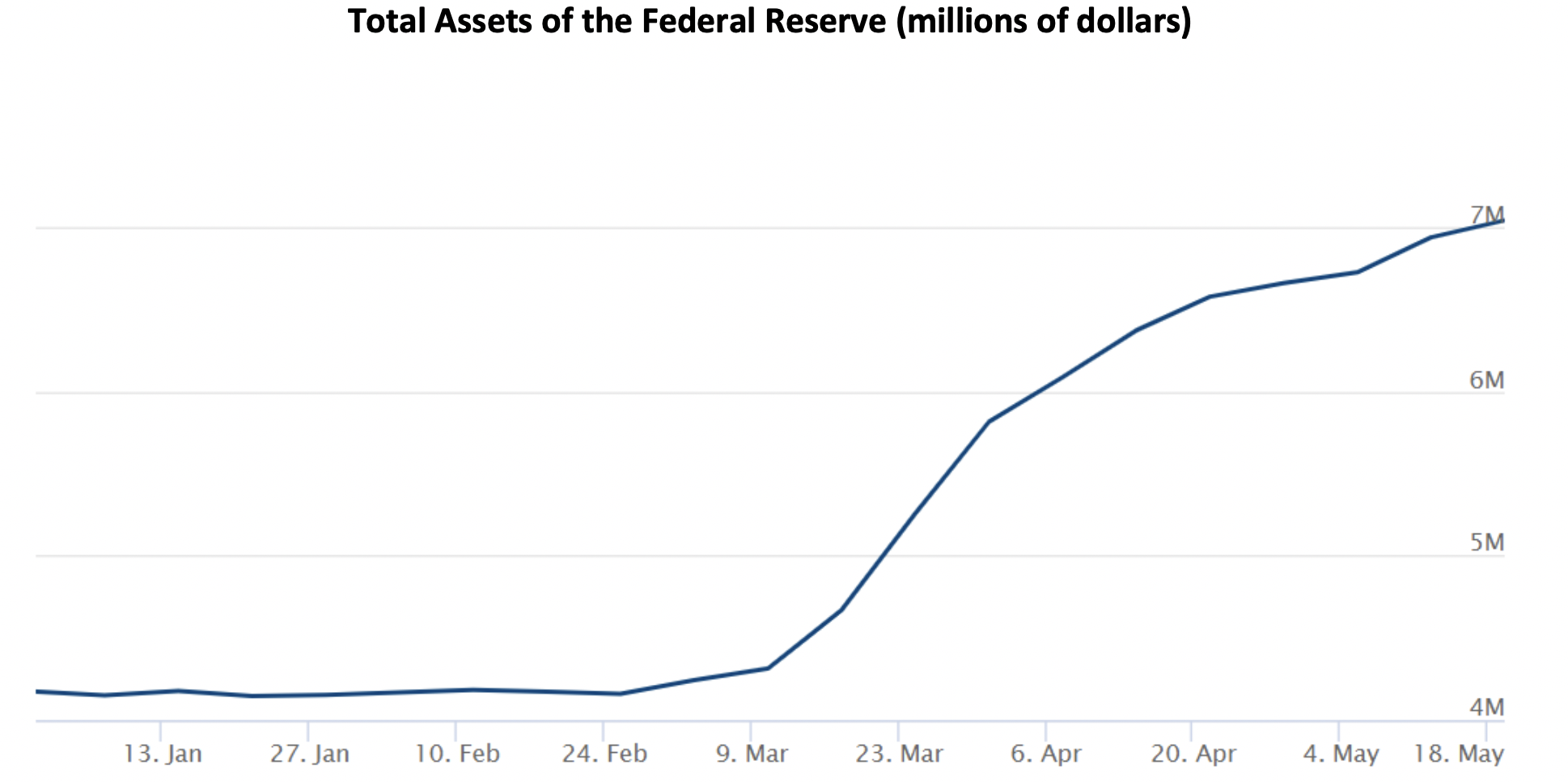

In the past two months the Federal Reserve’s has expanded from a little over $4 trillion at the beginning of this year to almost $7 trillion, as the US central bank has spent up to $75 billion daily purchasing US government bonds.

Source: Federal Reserve

Druckenmiller explained that drastic cuts to earnings projections have not mattered as the Fed’s multi-trillion-dollar bond-buying program has leaked into risk assets like equities. As investors sell these low risk assets to the Fed they have likely redeployed funds into higher risk assets, including high yield bonds and equities, regardless of the outlook for company earnings.

This has meant that US stock prices have been able to rise more than 30 per cent since the end of March, even as earnings forecasts for US corporates have fallen by almost 20 per cent. Moreover, the correlation between stock prices and earnings forecasts has been close to negative one – an almost perfectly inverse relationship.

US stock prices and earnings forecasts since the end of March 2020

Just as Druckenmiller cautioned that the liquidity effect dominates in the “intermediate” term, a study over the last two decades shows that in the long run the direction of corporate profitability is highly likely to dictate the direction of stock prices. In fact, the correlation between share prices and earnings forecasts since 2000 has been almost positive one – an almost perfectly direct link, and a stark contrast to the relationship over the short run.

US stock prices and earnings forecasts since 2000

The divergence between stock market prices and company earnings in the past two months should warrant near-term caution from long-term investors, who seek to compound wealth over decades. Many such investors are clients in the Montaka and Montgomery Global strategies. They can take comfort in the defensive positioning of these funds, with low net market exposure and high cash holdings, respectively. Rather than chase short-term liquidity-fuelled bounces, we are focussed on protecting capital at a time when fundamentals have diverged significantly from prices and the possibility of substantial downside has risen.