Australian toll road operator, Atlas Arteria (ASX:ALX), has announced a new, simpler ownership structure that should benefit the company and its shareholders. The deal includes the separation from Macquarie Group – thus ending ongoing management fees to the ‘silver doughnut’ – and an increased stake in APRR, Europe’s fourth-largest motorway operator.

Atlas has investments in three different toll roads located in France, Germany and USA and started life as Macquarie Atlas. The company was started and managed by Macquarie Group but from 1 April 2019, it has been managed by an external management team but as the corporate structure is rather complicated (not unusual for Macquarie vehicles), Macquarie was still getting fees of around $15 million per year for managing Atlas’s stake in the most valuable asset, the APRR motorway in France where Atlas own 25 per cent.

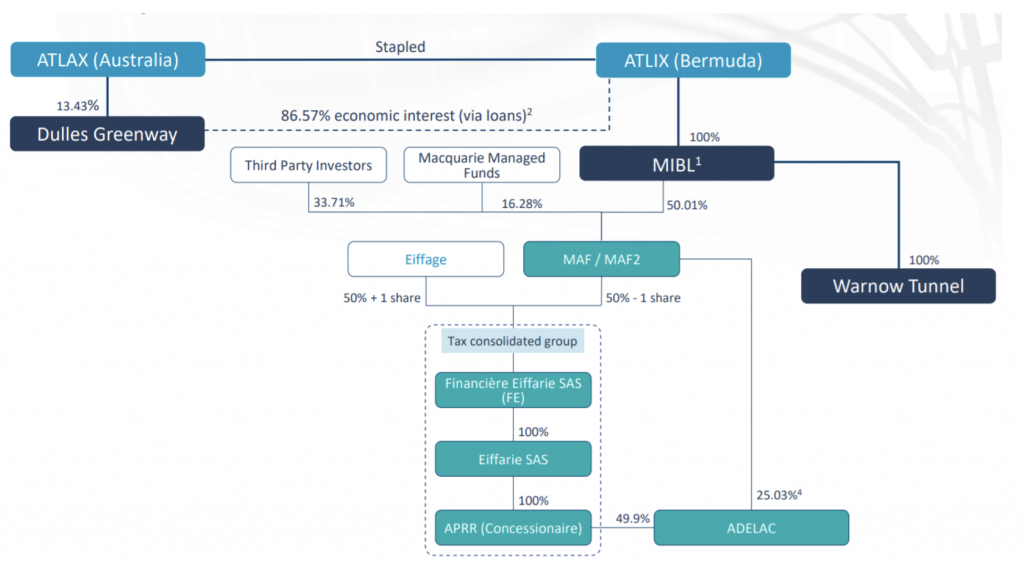

The new management team has been busy negotiating a complete separation from Macquarie. This has not been an easy task given the number of stakeholders involved. To get an idea, look at the organizational chart below:

I understand if you find this chart difficult to make sense of (it took me a LONG time to fully understand the intricacies) but for today’s purposes, let’s focus on the MAF/MAF2 box and its surrounding boxes and identify the key stakeholders involved.

Key Stakeholders

In total, this makes up six different stakeholders (counting Macquarie Group and the Macquarie Managed Funds as separate entities as there are different decision makers with different responsibilities involved). As anyone who has been involved in any negotiation knows, arriving at an outcome that satisfies everyone is not easy and the difficulty increases exponentially the more parties are involved!

My superficial outside assessment of the different parties’ main objectives is as follows:

Atlas Arteria:

Eiffage:

Macquarie Managed Funds:

Third party investors:

Macquarie

The situation is further complicated by:

As you can understand, this makes for a very complicated situation with many moving parts and many parties with varying motivations that need to be satisfied for a deal to occur. It is therefore very impressive to see the recent announcement that the new management team of Atlas Arteria has managed to negotiate a deal that we believe satisfies everyone including the shareholders of Atlas Arteria!

Atlas Arteria Deal

The deal structure in short is:

As far as we can see, this is a good deal for everyone and it is also something we think will be value accretive to Atlas Arteria’s shareholders.

The effective valuation that Atlas is buying the shares in APRR is around 10.3x EV/EBITDA which we think is very fair for the asset given the growth profile and remaining concession life.

Eiffage gets to increase its effective stake in APRR through its 4 per cent stake in MAF/MAF2 and also gets rid of the Macquarie Managed Funds which have been holding back further investments in APRR.

Macquarie gets compensated for the loss of management fees.

The Macquarie Managed Funds get closer to being able to wind up which will potentially trigger performance fees to Macquarie.

Third party investors do not see their stake in APRR go up but will likely benefit from an increased valuation of APRR as both the risk profile for the asset reduces with fewer stakeholders and the opportunity for further investments increased.

Overall, we see this as a good deal and congratulate Atlas management on negotiating it!

The Montgomery Fund and Montgomery [Private] Fund own shares in Atlas Arteria. This article was prepared 26 November with the information we have today, and our view may change. It does not constitute formal advice or professional investment advice. If you wish to trade Atlas Arteria you should seek financial advice.