With 2020 almost now behind us, I thought it was worthwhile looking at the year that was. It’s safe to say this year is unlikely to be forgotten for everyone, and not just those invested in equity markets. After a very strong January, investors and markets grappled with the uncertainty and severe volatility brought upon by COVID-19’s spread around the world.

Many historic records were set and broken, with March being particularly noteworthy for swings in sentiment including:

We also had a very strong rebound in April as central banks unleashed liquidity to prevent a financial meltdown, while governments looked to support households with unprecedented budget deficits.

Other notable developments in 2020 include:

There was also an enormous level of corporate activity, as companies looked to shore up their balance sheets while a number of companies looked to capitalise on elevated liquidity by listing their businesses on the ASX.

Australian 10-year bond yields – having started off the year at approximately 1.4 per cent, leaves 2020 at around 1 per cent albeit after bottoming out at 61 basis points in the depths of the COVID-19 crisis. It remains to be seen whether 10-year bond yields stage a recovery as growth expectations improve following a year “on-pause” due to COVID-19.

In terms of aggregate PEs, we have:

Albeit the composition is vastly different, as the financials (mostly banks) trade at a significant discount to the broader industrials market, as does resources.

Market movers

In terms of index constituents, here are some of the moves seen over 2020:

Source: Bloomberg, MIM

The top movers this year have largely been the miners, as well as some large-cap tech. After starting the year off as laggards (given the initial wide-spread impact of Coronavirus was in China), the large-cap miners have posted strong returns due to a much stronger iron ore price than expected as the Chinese government has reverted back to Fixed-Asset investment to restimulate the economy post the COVID induced slowdown, and some minor supply disruptions helps already bullish sentiment.

Source: Bloomberg, MIM

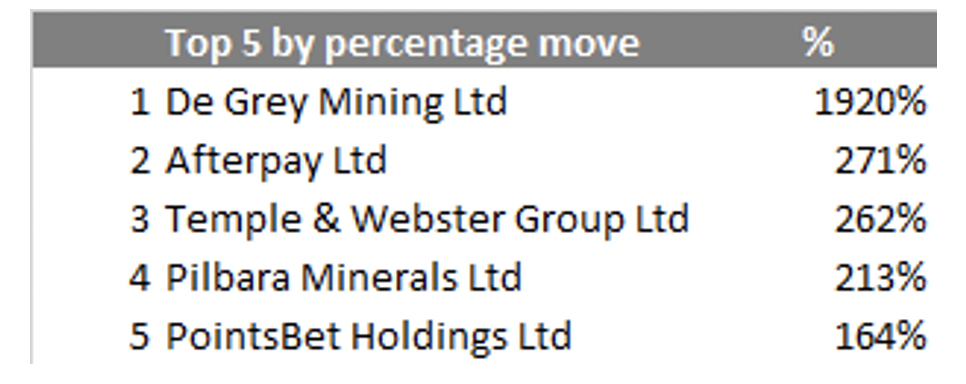

The top mover for 2020 is De Grey Mining, which entered the ASX300 in September following a meteoric share price rise driven by exploration success at its Hemi Gold project in Western Australia. Afterpay is next on the list, albeit its 271 per cent return does little justice to its share price journey over the year.

Source: Bloomberg, MIM

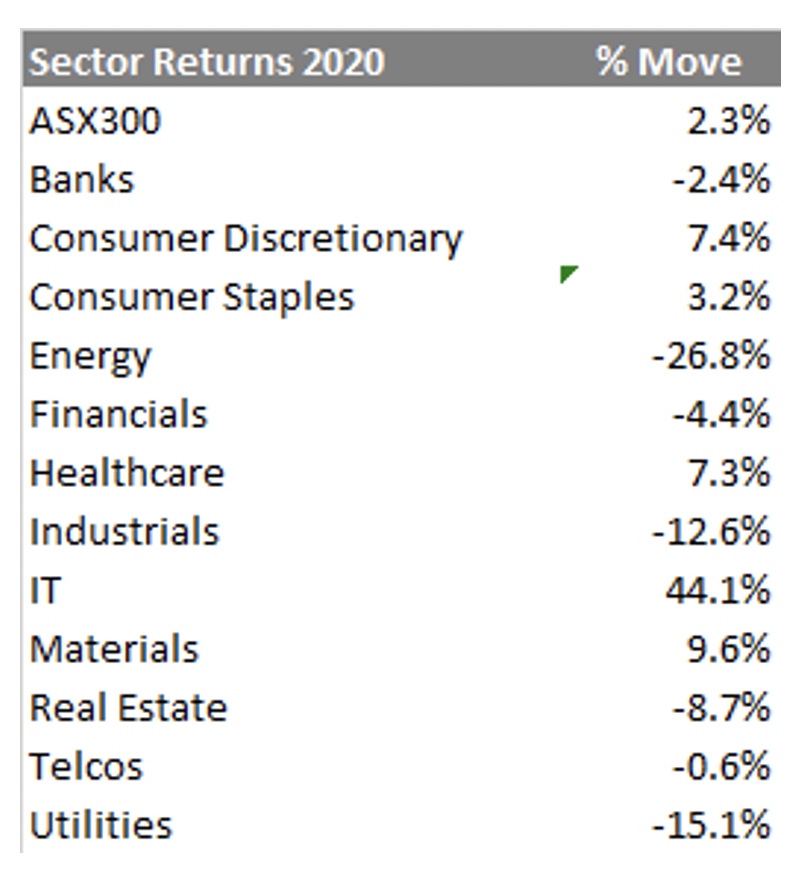

Like Healthcare and CSL in 2019, the outperformance of the IT sector was largely driven by the two heavyweights Afterpay and Xero.