There has been a lot written about the death of value investing, and how growth investing has outperformed significantly over recent years. However, it is important to distinguish the difference between the traditional concepts of “value” investing – i.e. capital intensive industries trading at low price-earnings or other similar ratios (including price / book), with the concept of “valuation” – determining the present value of an asset.

The concept of valuation is subjective to the valuer, but it transcends all form of investing. In its purest sense, value is reflected in the last transacted price, as it reflects the middle ground between a willing buyer and a willing seller at that point in time. As an individual, you may not agree with the price, but there may be someone out there who is willing to take a different view – this is what makes the market.

However, there are times when the last transacted price may not be a meaningful reference point to determine a future value outcome despite the human tendency to do so – a potential form of anchoring bias. The example of Pro Medicus (PME:ASX) is a useful case study to illustrate when the concept of valuation – rather than price – becomes important.

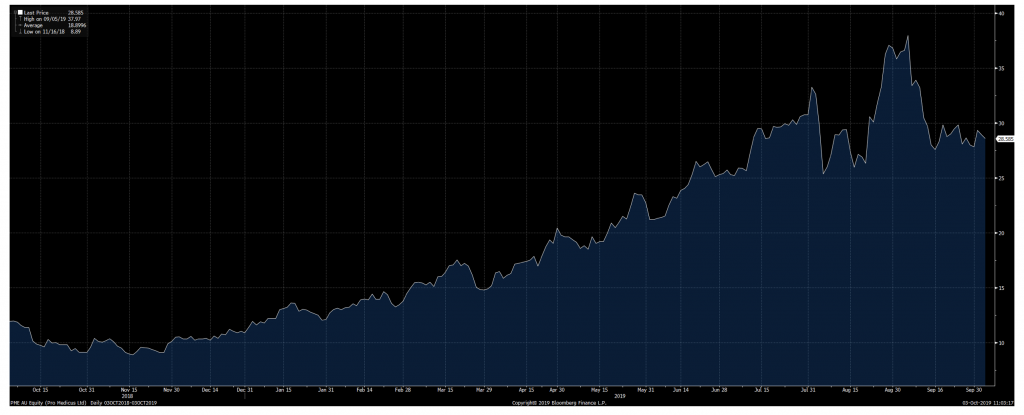

PME’s share price performance

PME has been one of the top performers on the ASX300 this year, with the share price peaking at $38/share, good for a 218 per cent increase over the past 12 months. However, the stock was one of the worst performers in September, with the current share price of around $29/share equating to a 24 per cent fall from its recent highs. The fall was for the most part triggered by a small sell-down of shares by the founders (around 2 per cent of shares on issue).

Pro Medicus share price performance

Source: Bloomberg

Given the share price fall, does this suggest PME is now good “value”? Using the recent highs as a guide – the shares are 24 per cent “cheaper”– and the fact there’s been no major change to underlying business fundamentals, would suggest a closer look is warranted.

However, instead of looking at where it has come from, it is important to ask was that the “right” share price in the first place. A share price fall may trigger initial interest, but having a valuation overlay helps put price moves in context.

When valuation matters

Valuation overlays help to provide an anchor for when a share price may suggest good “value” to the incremental investor, given a certain set of projections. i.e. would the buyer expect to reliably make a profit from acquiring shares at the prevailing price regardless of investing strategy – whether it be earnings growth, company re-rate, price momentum, greater fool theory, or any other method. Note how this is completely independent to the concept of being a growth or value investor.

This anchor applies for any sort of valuation methodology – whether it be revenue or earnings multiples, balance sheet ratios (price / book) or discounted cash-flow analysis. While subjective, it is these valuation metrics that help determine your view of a “floor” price on a given set of assumptions.

Despite having a superior product to competitors, the concept of valuation is separate to the perceived quality of a business. At a forecast PE of 119x for 2020, and given the size and nature of PME’s contracts, it would have likely taken a number of years before the projected growth of PME’s earnings could justify the prevailing valuation metrics for the majority of investors.

Potential to forgo gains, but process is important

The potential downside to this argument is that strict adherence to these philosophies may result in taking profits early – in this case, one could make a reasonable argument about PME’s stretched valuation metrics at $25/share based on the projected level of earnings growth.

However, these same stretched metrics would have only gotten more stretched at $30/share, $35/share, and eventually $38/share, so selling at $25/share would have resulted in forgoing 50 per cent of the upside.

One exercise that may help mitigate sellers’ remorse is to back-solve the revenue and earnings growth projections that are implied in the share price – compared to your projections – through a relative value lens, to determine whether the assumptions may appear reasonable to the incremental investor.

While this process may inevitably lead to taking profits earlier than what hindsight will determine, this discipline should help limit the downside as a result of an unexpected change in market sentiment to the shares.